When it comes to property investing in Australia, the “holy grail” for many is a structure that offers the asset protection of a trust without losing the immediate tax benefits of negative gearing.

If you hold a property in a standard Family (Discretionary) Trust, any rental losses are usually “trapped” inside the trust. This means you can’t use those losses to reduce the tax on your salary. However, a Negative Gearing Trust (sometimes called a “Fixed Entitlement” or “Hybrid” structure) is designed specifically to bridge this gap.

Here is a blog post by Rider Accountants that explains why this might be the right move for your portfolio.

Asset Protection Meets Tax Savings: Why Use a Negative Gearing Trust?

For the serious property investor, choosing how to hold your assets is just as important as what you buy. Traditionally, investors face a dilemma:

Buy in your own name: You get the tax benefits of negative gearing, but your property is exposed to personal legal risks and creditors.

Buy in a family trust: You get excellent asset protection and estate planning flexibility, but your negative gearing losses are “trapped” until the property becomes profitable.

But what if you could have both? Enter the Negative Gearing Trust.

What is a Negative Gearing Trust?

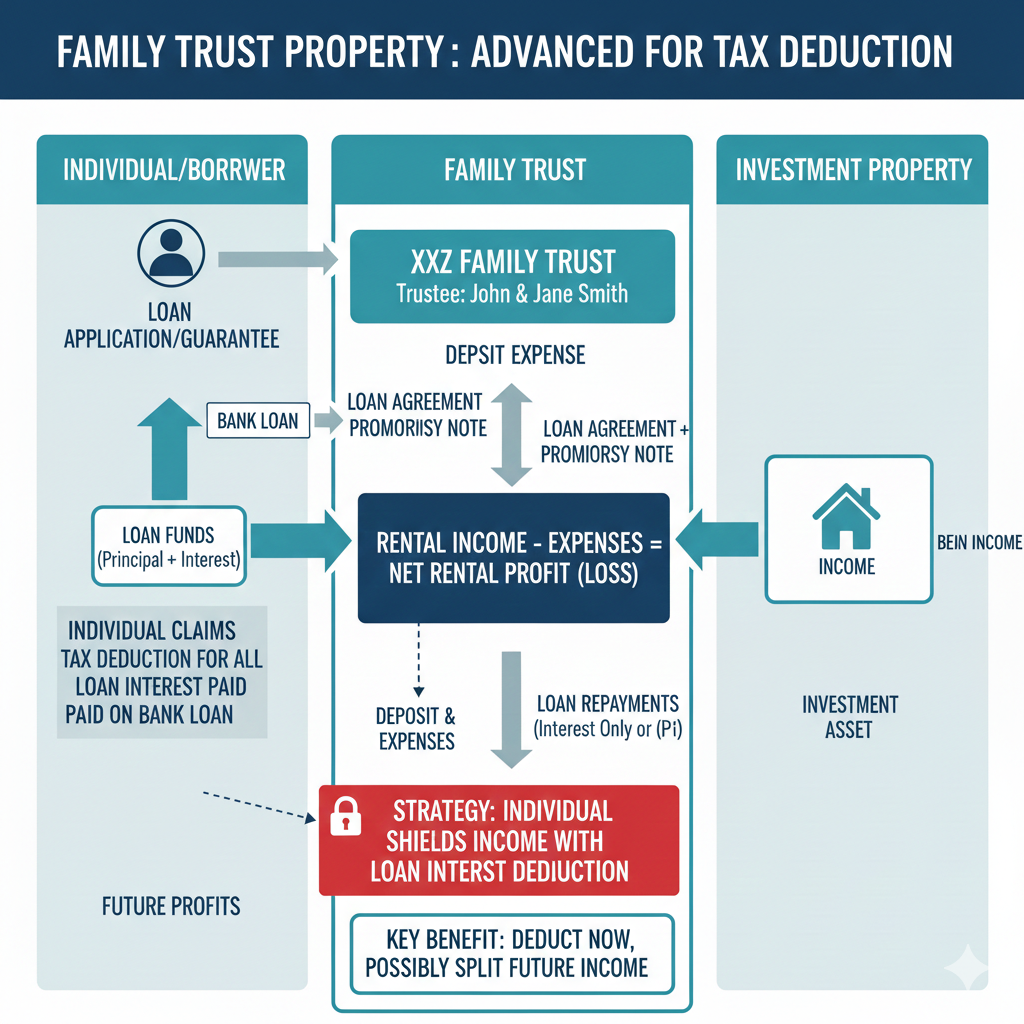

A Negative Gearing Trust is a specialised trust structure designed to satisfy the Australian Taxation Office (ATO) requirements for interest deductibility while keeping the asset itself within a protective trust environment.

In this arrangement, the investor typically borrows funds in their own name and on-lends them to the trust (or buys specific units in the trust) under very specific terms. This allows the individual to claim the interest expense on their personal tax return, effectively negatively gearing the investment.

4 Reasons Property Investors Use This Structure

1. Superior Asset Protection

The primary reason to use any trust is security. Because the property is legally owned by a trustee (often a shelf company) rather than you personally, it is generally shielded from personal creditors. If you are a business owner or a professional in a high-risk industry (like medicine or law), this “firewall” between your personal liabilities and your wealth is essential.

2. Immediate Tax Deductions

Unlike a standard discretionary trust where losses stay locked away, a correctly structured Negative Gearing Trust allows the individual beneficiary to claim the interest costs against their high-tax salary. This can result in significant tax refunds, which helps manage the cash flow of holding the property during those early, expensive years.

3. Future Income Splitting

While the trust acts like a “fixed” structure during the negative gearing phase, it can be designed to offer flexibility once the property becomes “positively geared” (profitable). At that point, the trust can potentially distribute surplus rental income to other family members in lower tax brackets, such as a spouse or adult children, significantly reducing your family’s overall tax bill.

4. Simplified Estate Planning

Properties held in a trust do not form part of your personal estate. This means that if you pass away, the property doesn’t necessarily need to be sold or transferred via a will, which can trigger massive Stamp Duty and Capital Gains Tax (CGT) events. Instead, you simply change the “control” of the trust, allowing your wealth to pass to the next generation seamlessly.

5. Why Use a Negative Gearing Trust?

Well it depends. Firstly, for asset protection. The asset will not be held in the individual’s name but instead in the trust. As such, the equity in the asset acquired in the trust could be substantially protected against claims against the individual especially if there is a corporate trustee of the trust. Secondly, individuals use it to obtain a tax deduction for borrowings made in their own name. Generally, individuals cannot claim a tax deduction for interest expenses incurred for assets held in discretionary trusts. A negative gearing trust is a special type of trust where an individual may be able to obtain a tax deduction for interest expenses incurred on the bank loan even though the asset is in the discretionary trust. The net income in the trust will be substantially less than the interest payable on the loan in the early years. This means the individual will get a tax deduction for substantially all of the interest payable on the loan. Thirdly, individuals use a negative gearing trust to give them flexibility to deal with surplus income and capital of the trust. Under a negative gearing trust structure any income that exceeds the interest payable on the loan can be distributed to a discretionary trust. From this discretionary trust the trustee can then distribute that surplus income in any manner it pleases. Similarly, any capital gains can be distributed to any beneficiaries under the trust. It doesn’t have to be the actual individual that made the initial loan to the trust. This is the case provided they recouped all the interest paid to the bank.

{kind=link}

{kind=link}

{kind=link}