- Accountants & Finance Brokers est.1999

- (02) 89578454

- team@rideraccountants.com.au

I have a Trust and want to borrow money from the bank

October 29, 2024Should I Open a Self Managed Super Fund (SMSF)?

January 16, 2025GST and Airbnb - Charge GST on short-term rentals or not?

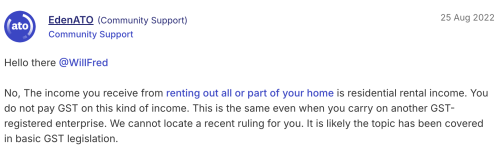

For most AirBNB and other short term rentals, you will be renting out residential property. GST doesn’t apply to residential rent, however you may need to report and pay GST in some situations, for example.

When GST was introduced in 2000 it was never intended to apply to residential rent. Therefore, you are not liable for GST on the rent you charge, and you can’t claim any GST credits for associated expenses. This applies even if you carry on another GST-registered enterprise.

Generally, rental income from residential premises is classed as an input-taxed sale and you don’t include GST in the rent you charge. An input taxed sale is a GST free sale where you cant offset GST on purchases you make in producing the rental income.

Short Term Rental – Residential Premises

Section 195-1 of the GST Act clarifies what is meant by “residential premises”. That section provides that the term “residential premises” refers to any land or building that:

- is occupied as a residence or for residential accommodation; or

- is intended to be occupied, and is capable of being occupied, as a residence or for residential accommodation,

regardless of the term of the occupation or intended occupation. It’s also worth noting a supply of residential premises may consist of a single room, or apartment or a larger complex consisting of rooms or apartments.

So the basic GST legislation released in 1999 indicates that you cannot charge GST on renting out a residential premises even if that involves short term rental on Airbnb, Stayz or Booking.com. There appears to be no direct ATO rulings related to running a STR business that rents residential premises aside from commercial residential premises which is dealt with in the next section.

A short term rental host’s supply of their apartment or house by lease, hire or licence is an input taxed supply of residential premises to be used predominantly for residential accommodation under paragraph 40-35(1)(a) of the Goods and Services Tax Act 1999.

Short Term Rental – Commercial Residential Premises

Some AirBNB hosts may have multiple properties that they rent out on short-term stay and these properties may include “commercial residential premises” (i.e. properties built specifically to rent out). In tax ruling GSTR2012/6, ATO provide detail explanation of commercial residential premises included a hotel, motel, inn, hostel, caravan park, boarding housed or anything similar. ATO clearly states that a single home let on a short-term basis is not a supply for commercial residential premises.

Division 87 of the Goods and Services Act 1999 specifically addresses the issue of stay length as it relates to commercial residential premises. Short-term accommodation is when a guest stays for less than 28 continuous days, in which case you’re liable for GST of one-eleventh of the price you charge for the accommodation Long-term accommodation is defined under the GST Act – when a guest stays for 28 or more continuous days, in which case concessionary GST treatment applies

Common characteristics of operating premises as commercial residential premises (and therefore where GST applies) are:

- •

- Commercial intention

- The premises are operated on a commercial basis or in a business-like manner even if they are operated by a non-profit body.

- •

- Multiple occupancy

- The premises have the capacity to provide accommodation to multiple, unrelated guests or residents at once in separate rooms, or in a dormitory.

- •

- Holding out to the public

- The premises offer accommodation to the public or a segment of the public.

- •

- Accommodation is the main purpose

- Providing accommodation is the main purpose of the premises.

- •

- Central management

- The premises have central management to accept reservations, allocate rooms, receive payments and perform or arrange services. This can be provided through facilities on-site or off-site.

- •

- Management offers accommodation in its own right.

- The entity operating the premises supplies accommodation in its own right rather than as an agent.

- •

- Provision of, or arrangement for, services

- Management provides guests and residents with some services and facilities, or arranges for third parties to provide them.

- •

- Occupants have status as guests

- Predominantly, the occupants are travellers who have their principal place of residence elsewhere. The occupants do not usually enjoy an exclusive right to occupy any particular part of the premises in the same way as a tenant.

For hosts that have multiple AirBNB properties, you can see there are some grey areas since your AirBNB guests are considered to be guests and the host provides guest with services and facilities.

Ultimately, whether premises are commercial residential premises and where GST is applied is a matter of overall impression involving the weighing up of all relevant factors. While not an exhaustive list, factors that may indicate that premises are not a hotel, motel, inn, hostel, boarding house or similar premises include:

- (a)

- the operator and occupant agree for accommodation to be supplied for a periodic term (which may be for a period of months or years at a time), such as in a residential lease;

- (b)

- the operator and occupant document the condition of the premises under a written contract before the accommodation is initially supplied and when the occupant ceases to occupy premises;

- (c)

- the operator has the right to impose a cleaning fee on the occupant when the occupant ceases to occupy the premises;

- (d)

- the occupant is permitted, subject to the terms of the lease or licence, to alter the part of the premises occupied by the occupant, such as by attaching hanging devices on a wall;

- (e)

- the occupant is permitted, subject to the terms of the lease or licence, to keep pets in the premises;

- (f)

- the occupant must separately arrange and pay for the connection of a telephone, electricity, or gas service;

- (g)

- the occupant is responsible for the cleaning and minor maintenance of the premises, such as changing light bulbs in their room;

- (h)

- the premises are unfurnished; and

- the right to occupy the residential premises is supplied to the occupant in exchange for the occupant loaning an amount to the operator together with other fees.

While the accommodation provided through short term rental platforms such as Airbnb, Stayz and Booking.com for residential premises does display some characteristics of commercial residential premises, the supply of the accommodation through the single apartment or house is not sufficiently similar to a hotel, motel, inn, hostel or boarding house to be characterised as accommodation provided in a commercial residential premises. The fact that the platform or manager acts as agent in respect to several apartments or houses and offers accommodation in that capacity to several parties at once is not sufficient to characterise the supply a short term rental host makes to the guests through the manager as accommodation provided in commercial residential premises. For one the host does not reside at the premises and the premises has more residential semblance than commercial (kitchen, laundry, car garage, dishwasher, no-onsite management). It’s fair so say though this is a grey area and one that way be further clarified by the ATO in in the future (this article for reference was written in November 2024).

Short Term Rental – Commercial Premises

Irrespective of whether commercial premises are rented short or long term, they are considered to be taxable supply meaning they ARE subject to GST.

If you undertake short term rental of commercial premises such as office, industrial or multi-family premises, and you’re registered or required to be registered for GST, you:

- are liable for GST on the rent you charge

- can claim GST credits on purchases made relating to leasing your property, for example the GST included in the managing agent’s fees

- you may be able to claim the GST included in rent you pay.

Airbnb short term rental business with multiple properties

But what if you have an AirBNB or other short term rental and you earn over $75,000 in rental income? In any other business you are legally required to register for GST and charge GST as soon as you bill more than the $75,000 GST threshold. Does this GST tax threshold apply to AirBNB or other short-term rentals? When you’re working out your GST turnover you don’t include any input-taxed sales you make (residential rental income) to work out what your threshold is. If the rental income is the only source of business income you have, then you would not need to register for GST.

There are however more complex issues to consider. Some short-term rental marketing companies like Stayz may include GST in their charges. There may be cases, where your clients (especially business clients) may request a GST invoice and expect to claim the GST paid as they would in a hotel. For AirBNB customers in Australia, Airbnb service fees are subject to 10% GST. If you as the AirBNB host are registered for GST, you may not be charged GST on Airbnb service fees. However, you may still be required to declare GST on your GST filing.

It should be noted that you can’t charge GST on bonds you receive from your short term rental clients.

AirBNB Managers

There are some Airbnb businesses that focus on providing management services to Airbnb hosts or property owners. In this case the Airbnb managers are making a ‘taxable supply’ for the management services and must charge GST if the turnover of the business is over $75,000. Airbnb managers will issue tax invoices with GST for the hosting management component and also claim GST on the expenses of the business.

Summary

To summarise this somewhat long and complicated article, if you are an AirBNB host that earns less than $75,000 income you should not charge GST. If you earn more than $75,000 rent from Airbnb for residential premises you don’t need to register for GST as residential rent is an input taxed supply which also means you cannot claim the GST on your expenses and the rental income you receive does not count towards the GST threshold. This is the case even if you are carrying on an AirBNB business where you work full-time facilitating short term rentals and have multiple properties. If you are hosting commercial premises or commercial residential premises over $75,000 income per year then yes you must register and charge GST.

Summary of Short Term Rental Scenarios and GST

- STR Host or Manager earning less than $75,000 per annum for any property type --> No GST

- STR Host with Commercial Premises earning more than $75,00 per annum --> Yes GST

- STR Host with Residential Premises earning more than $75,000 per annum --> No GST

- STR Manager running a business and earning more than $75,000 per annum --> Yes GST (for the management fees only)

- STR Host with Residential Premises running a business and earning more than $75,000 per annum --> Yes GST (BUT for the management fees only)

- STR Manager with Commercial Residential Premises or Commercial Premises running a business and earning more than $75,000 per annum --> Yes GST (for the total invoice value)

Short Term Rental GST Examples

The following table will help short stay rental Airbnb hosts navigate the complicated world of GST:

- commercial residential premises such as a boarding house or caravan park YES GST

- farm stays YES GST

- residential houses and apartments NO GST

- retirement homes NO GST

- student accomodation YES GST

- boarding house NO GST

- camp style accomodation YES GST

- holiday apartments or houses NO GST

- apartments that are residential premises NO GST

- separately titled rooms with commercial support infrastructure YES GST

- boat for hire YES GST

- boat on a marina for residential living NO GST

AirBNB hosting tax implications can be much more complex than most hosts realise and it’s vital you have a specialist Airbnb (short-term rental) accountant on your team so reach out to Australia’s #1 Airbnb accountant Steven P. Rider who can help you navigate this complex tax law and help you stay compliant while maximises the return on your Airbnb investment. Call (02) 8957 8454 or email property@rideraccountants.co.au

{kind=link}

{kind=link}

{kind=link}